Huayang FY16Q1 Financial Result

| Huayang | FY16Q1 | FY15Q4 | FY15Q3 | FY15Q2 | FY15Q1 |

| Revenue | 142.6 | 152.1 | 155.5 | 139.5 | 136.5 |

| Gross Profit | 51.5 | 53.2 | 59.3 | 45.2 | 43.2 |

| Gross% | 36.1 | 35.0 | 38.1 | 32.4 | 31.6 |

| PBT | 40.2 | 42.5 | 43.2 | 35.2 | 32.6 |

| PBT% | 28.2 | 27.9 | 27.8 | 25.2 | 23.9 |

| PAT | 29.9 | 29.7 | 30.9 | 26.0 | 23.9 |

| Total Equity | 495.8 | 465.9 | 449.4 | 436.9 | 410.9 |

| Total Assets | 944.2 | 923.2 | 877.3 | 828.0 | 811.0 |

| Trade Receivables | 72.9 | 88.9 | 73.3 | 68.1 | 62.6 |

| Prop dev cost | 161.5 | 167.7 | 175.5 | 159.5 | 145.1 |

| Inventories | 10.5 | 9.9 | 9.8 | 9.8 | 10.0 |

| Other Current Assets | 200.7 | 189.6 | 180.3 | 157.0 | 165.6 |

| Cash | 62.6 | 40.9 | 44.1 | 43.9 | 27.0 |

| Bank Overdraft | 4.6 | 7.4 | 14.4 | 10.9 | 15.0 |

| Total Liabilities | 448.5 | 457.4 | 427.9 | 391.1 | 400.0 |

| Trade Payables | 135.1 | 141.5 | 118.2 | 120.4 | 134.5 |

| ST Borrowings | 78.1 | 78.6 | 82.2 | 75.9 | 74.2 |

| LT Borrowings | 195.4 | 192.1 | 187.4 | 161.0 | 165.2 |

| Net Cash Flow | 24.4 | 3.4 | -0.5 | 2.7 | -18.2 |

| Operation | 25.6 | 115.9 | 71.1 | 58.1 | 26.1 |

| Investment | -6.7 | -86.6 | -50.7 | -23.9 | -11.2 |

| Financing | 5.6 | -26.0 | -20.8 | -31.5 | -33.2 |

| Dividend paid | 0 | 44.9 | 31.7 | 13.2 | 13.2 |

| EPS | 11.32 | 11.25 | 11.72 | 9.84 | 9.07 |

| NAS | 1.88 | 1.76 | 1.70 | 1.65 | 1.56 |

| D/E Ratio | 0.43 | 0.51 | 0.53 | 0.47 | 0.55 |

| Unbilled sales | 660.8 | 701.9 | 733.3 | 717.9 | 756.4 |

I expect Huayang to post average quarterly net profit of RM25-30mil in its FY16, so its FY16Q1 net profit of RM29.9mil is not a surprise.

The main concern is the fact that Huayang just achieved RM81.7mil new sales in its FY16Q1 (Apr-Jun15), which is only 16% of its target annual sales of RM500mil, or 18% of FY15 overall sales of RM460mil.

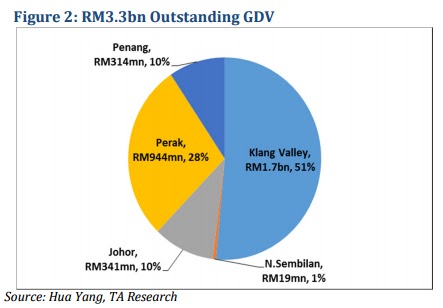

As a result, unbilled sales drop to RM661mil from RM702mil a quarter ago.

Nevertheless, latest sales were achieved without any launch of new project in the last 2 consecutive quarters. So the RM81.7mil figure are not too bad I think.

Huayang is unlikely to launch new project in current quarter of FY16Q2 (Jul-Sep15). Upcoming project Mines South will probably be launched in the end of CY15.

Targeted new launch for FY16 remains at RM633mil. Huayang still keeps its FY16 sales target intact at RM500mil, with RM426mil of already-launched projects available for sale.

Take-up rate of its final phases at One South has been poor so far. Sales of Cube and Zeta Residence improve slightly to 36-39% from 20-29% in previous quarter.

Citywoods's take up rate is even worse at 31% so far, up from 25% a quarter ago despite attractive selling price at RM500-600 psf compared to other high-rise projects at RM700-1000 psf in Johor Bahru, according to TA Securities.

While Huayang's financial results in FY16 should remain good, it certainly needs to improve its sales to at least RM500mil a year to sustain this performance.

In near term, its Klang Valley projects such as Mine South and Puchong West will be key.

The remaining unsold units at One South should get a boost from the proposed MRT2 route which has a station right opposite One South across the KL-Seremban Highway. A dedicated link bridge between the MRT station and One South has been proposed.

Meanwhile, the management will continue to acquire strategic land to expand its GDV.

Huayang's TTM EPS stands at 44.1sen. At share price of RM1.90, it is currently trading at PE ratio of merely 4.3x.

Huayang paid 12sen dividend for its FY14, which means a 38% payout ratio. If it decide to pay 35% in FY15, then it will be total 14.5sen.

It has given 5sen for FY15, and final dividend should be declared at the end of this month.

I think it is more likely to pay out 30% which means 12.5sen in FY15. If this is the case, dividend yield will still be an attractive 6.6% at current share price.

althoug i dislike prop right now, but pe 4 seems incredible cheap for Huayang. They hv a young n energetic ceo

ReplyDeleteAnd then i saw their one south, very modern and firm design,

can tell their strike a good balance between good design n cost control.

And then their market position is good, try not to fight direct with those Ecoworld, IJM selling "dream" house, but selling added value house with acceptable price, another word 性价比高。

Ya, a good management team is important. Just hope that they can acquire more strategic and yet cheap landbank :)

DeleteSeem prop sector is slowdown. After O&G. Following may be banking, retail...

ReplyDeleteHi Ali. I also think that banking should follow, then may be KLCI...

DeleteNot sure how long property slow down will last, probably another 1-2 years?

ReplyDeleteProbably after the next economy crisis?

Deletei dun expect the take up rate will improve in the coming days, but i hope the cost reduction will drive the profit growth.

ReplyDeleteU knw la, now China econ slows down, there will be more overcapacity of steel, then there will be more steel dumping to Malaysia.

Cheaper steel means cheaper building cost for Huayang, then the concrete price will also down.

Do u agree with me, BD?

Not sure about the China effect, but construction cost may go up after GST...

Deleteaiya, gearing almost a half, i better dun touch

ReplyDelete