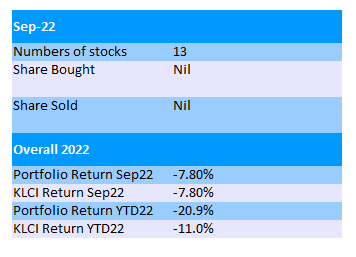

Summary For September 2022

The month of September is not a good month for stock market after a brief rebound in August. KLCI tumbled 7.8%, exactly the same as the performance of my portfolio in Sep22.

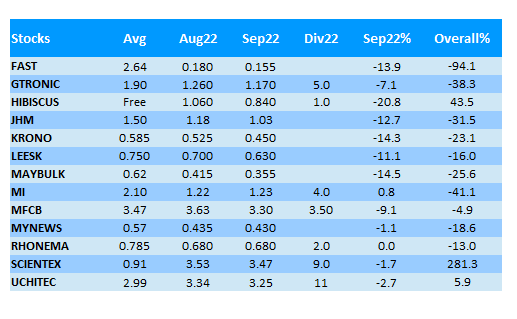

The worst performer is Hibiscus, which fell 21% in one month, followed by Maybulk, Krono, JHM & LeeSK which suffered more than 10% loss.

Overall year-to-date, accumulated loss since the start of the year has reached 20% for the first time.

Three companies in my portfolio announced their quarter results in September.

Krono's FY23Q2's result (PAT RM3.1mil, EPS 0.44) is not within my expectation, but not too bad either. Net profit increased 40% QoQ but dropped 40% YoY.

However, YoY, the EBIDTA in this quarter was comparable at RM10.5mil. The net profit was mainly dragged down by 30% higher depreciation charge.

Contribution from EDM infrastructure technology segment is still weak in the first half of FY23. Whether it can play catch up in the remainder of FY23 remains to be seen.

Nevertheless, its revenue growth trend continues and almost touched RM4bil in FY22. Its recent FY22Q4's revenue was its record high at RM1.1bil, while PATAMI stood at RM125mil (EPS 8.06sen).

Its expansion plan continues with a new blown film plant in Chemor expected to be completed by CY22Q3 while a new robotic stretch film plant in Shah Alam is expected to be completed by CY22Q4.

Scientex packaging's acquisition spree continues after the pandemic. Through Scientex Packaging (Ayer Keroh) Bhd, which was previously Daiboci, Scientex has acquired 80.2% stake in Taisei Lamick Malaysia Sdn Bhd (TLM) for RM63.8mil.

TLM was previously listed on Bursa Malaysia as Malaysia Packaging Industry Berhad (Maypak) and was taken private in 2017 when Japanese company Taisei Lamick Co.Ltd bought over the company.

Taisei Lamick is said to be the market leader in Japan for liquid and paste packaging system.

In its latest FY22 ended in Mac22, TLM which has its manufacturing site in Cheras, reported a revenue of RM61.7mil and net profit of RM1.34mil.

Its principal activity is manufacturing and sale of printed and laminated flexible light packaging materials and the sale and lease of machinery under the "Dangan" brand.

This type of packaging is mainly used in the fast growing F&B and FMCG products.

However, Scientex will transfer the Dangan machinery business (high speed auto filler for liquids and pastes) back to the vendor which I think makes sense.

The acquisition was announced on 2nd Sep22 and has been swiftly completed on 30th Sep22.

As for property segment, unbilled sales is at RM1.3bil (FY22Q4) compared to RM1bil in FY22Q3 despite a surge in property revenue in FY22Q4. This looks promising indeed.

Scientex's total borrowings of RM1,171mil might seem to be high compared to its cash of RM191mil. Net debt to equity stands around 30% though.

Its operating cashflow is strong at RM738mil in FY22, and RM700mil in previous FY21. The bank borrowing is mainly due to its relentless land banking activity which I think is OK.

MyNews's FY22Q3's result was better than my expectation. Its FY22Q3 bottom line improved tremendously from RM10.2mil loss (LATAMI) in preceding FY22Q2 to only RM1.4mil loss.

Revenue improved 20% from RM141mil to RM170mil in the same period of time.

The loss in its FPC has reduced to RM1.93mil from RM2.49mil too due to higher utilization rate at 60%. It is likely to turn profitable soon by FY23Q1 (Nov22-Jan23).

At the end of Sep22, there was 462 myNEWS outlets (including 16 myNEWS Supervalue), 124 CU outlets and 13 WH Smith stores.

With such result in FY22Q3, I can anticipate a profitable FY22Q4, hopefully.

In early Oct22, Hibiscus has given up its fight and agreed to pay sales tax to Sabah government, amounting to RM85.7mil.

Hibiscus decided to include this tax into its FY22Q4 ended in Jun22. Together with a RM125.5mil reversal of prior tax provision with IRB which will also be included in FY22Q4, the profit for full FY22 will be revised upward by RM39.8mil.

This means that Hibiscus will start its FY23 (from Jul22) clean without those one-off items. However, future sales tax to Sabah state government will reduce its profit from North Sabah PSC & Kinabalu PSC by ~5%.

Its upcoming quarter results might be fluctuating up and down depending on the timing of oil uptakes, especially with the newly acquired assets.

I think FY23Q1 might not beat FY22Q4. Brent oil price is trending down from USD120 in Jun22, only to be supported by OPEC+ output cut recently. Currently it stays above USD90 per barrel.

We know that crude oil price won't stay high for a long time. It will certainly drop to below USD60 dome day in the future. Is it wise to hold Hibiscus's shares?

Gtronic will announce its FY22Q3 quarter result later this month. This will mark the first result since it lost its pioneer status with tax incentive since Jun22.

Its previous tax rate was merely around 5%. How will the bottom line look like when the usual tax rate kicks in?

At slightly above RM1 now, its share price is even lower than during the peak of Covid-19 bear market.

Malaysia's Budget 2023 has been announced but I don't have any good or bad feelings for it.

Besides, we will have our 15th general election before 9th December after the Parliament was dissolved on 10th Oct22.

Stock market reacted negatively to it but if a strong government can be elected, it should be a good news.

However, the problem is that the chance of forming a strong government in federal level and certain states seem small. We might still see many frogs jumping here and there.

The main difference in this upcoming GE15 is that the voting age has been lowered to 18 from 21 years old, and eligible voters will be automatically registered.

So, there will be more youth participating in the upcoming general election, just that we are not sure how many voters are willing to travel back to their hometowns in order to cast their votes.

There are still lots of uncertainty when we step closer to the end of year 2022.

Other than the general election locally, Ukraine-Russia conflict, inflationary pressure worldwide and the possibility of global economy recession is still looming.

For my portfolio, the chance of escaping loss in year 2022 is almost impossible. I just hope that I can minimize the annual loss to below 20%.

No comments:

Post a Comment