Summary For May 2023

Portfolio @ End of May23

KLCI dropped 2% in May23 while my portfolio dropped even more at 4%, reducing the YTD gain to merely 2.7%.

Tech related stocks seems to suffer this month, with MI leading the pack by falling 15.8%. JHM & Krono both fell by 7%.

Nevertheless, Gtronic still managed to register a 7% gain in the month.

Both Hibiscus and Maybulk also dropped by a massive 10%.

Finally I have sold all my Uchitec shares.

Initially when I first bought its shares, I didn't expect too much from it. I just saw it as a fixed deposit with limited downside.

After holding it for 2 years and 3 months, the return of 30% is very good to me especially when other tech stocks are making loss.

This is mainly due to its fat dividend payout.

I sold Uchitec because of anticipated lower net profit after the expiry of its tax incentive.

Anyway, Uchitec released a very good net profit in its latest FY23Q1, due to a RM11.3mil gain from land sale.

Without this one-off gain, its PBT will still match preceding quarter of FY22Q4 but the significantly higher tax rate will eat up its net profit.

I'm not sure whether I made the right decision to sell Uchitec. I regret selling BAuto in 2020...

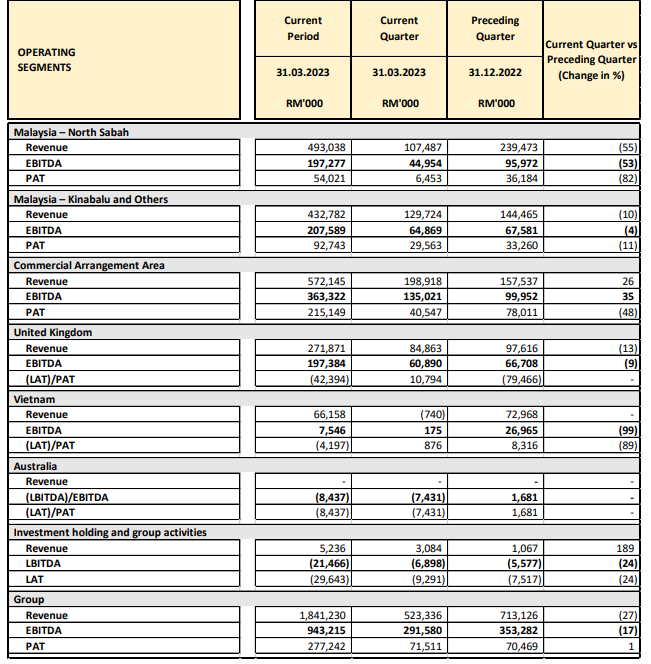

Hibiscus FY23Q3 revenue and net profit of RM523.3mil and RM71.5mil (EPS 3.55sen) respectively are still below expectation for 2 quarters in a row.

This set of result is not as good as what I expected.

Second interim dividend of 0.75sen was declared, bringing total dividend to 1.5sen so far in FY23.

JHM posted revenue of RM90.1mil and PATAMI of RM1.75mil (EPS 0.29sen) in FY23Q1.

Compared QoQ, even though revenue picked up by around 4%, PATAMI dropped by 20% due to increased costs, lower sales from industrial segment and unfavourable forex.

The management guided that the demand outlook for its automotive lighting segment remains healthy with the transition of projects from the qualification stage to production progressing as per schedule.

It will also start the assembly of rear combination lamp for a local car company by end of Q3 2023.

However, its industrial segment is not expected to turnaround so soon.

Analysts seem to be optimistic about its prospect going into FY24 though.

MFCB FY23Q1 result is disappointing as its PATAMI dropped to RM70.5mil (EPS 7.46sen) from RM95.2mil in preceding quarter.

Revenue and profit from its hydropower plant dropped significantly due to onset of dry season and scheduled annual turbine maintenance in Feb/Mac.

Performance of resources and packaging segment actually improved QoQ.

The net profit in this quarter was also affected by tax penalty of RM14.9mil and RM11.4mil one-off provision of income tax.

Without all these, its FY23Q1 result is actually not too bad.

LEESK registered revenue and net profit of RM29.7mil & RM3.4mil (EPS 2.13sen) respectively for its FY23Q1.

This is not a spectacular result but it looks like the best result compared to other stocks in my portfolio.

Domestic sales still look good but export sales continue to disappoint.

However according to AmInvest, the management guided that there could be recovery in export sales in FY23Q3 as the group received more enquiries compared to previous years.

The most anticipated financial result for me this quarter is T7Global's FY23Q1 result.

Sadly, it didn't turn out to be a good one with just RM4.24mil of PATAMI (EPS 0.56sen) under revenue of RM94mil.

The quarter report did not mention anything about its Bayan MOPU which was expected to contribute to its profit in Q1.

Luckily there are analysts helping to clear the clouds by reporting that there was a delay in its Bayan MOPU operation to Q2 of FY23.

The construction progress of KLIA baggage handling system has reached 12% completion while there was a pick up in orders in its aerospace segment.

While stock market indices in US keep going up, ours seem to go down the drain.

YTD loss in KLCI has already reached 7.25%.

We will have state election soon in July in which investors might have one eye on it.

Hopefully in the second half of 2023, when the interest rate hike cool down, we will welcome a new round of bull run.

No comments:

Post a Comment