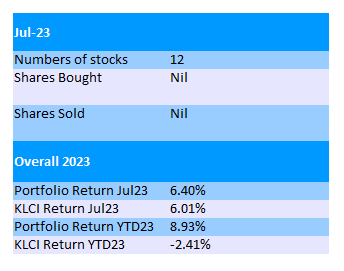

Summary For July 2023

Portfolio @ End of Jul23

July 2023 was a rather good month for stock market as tech stocks led the way.

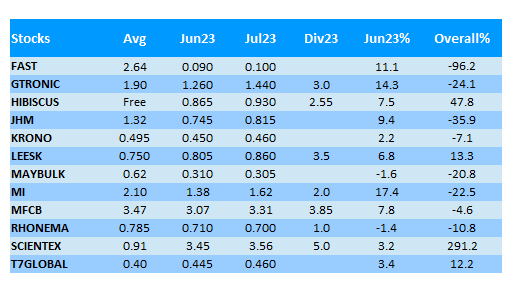

MI's share price jumped 17% while Gtronic gained 14%. JHM was not far behind with a 9.4% gain in the month.

Overall my portfolio improved by 6.4% in parallel with an impressive 6.0% gain in KLCI in the month of Jul23.

In this month, bonus shares of Krono was ex-ed and there was no buy sell transaction for me.

Quarterly revenue of RM31.5mil is the lowest in "n" years. Net profit of RM7.1mil (EPS 1.06sen) is largely due to the forex gain of RM4mil.

Traditionally second half of the year will be better for Gtronic. Lets see whether this year will still be the same.

Its share price rallied from RM1 in May to RM1.70 in mid July, only to fall sharply after the latest result announcement.

I guess this should be the bottom for Gtronic. If the revenue continues to drop further, then really no eye see.

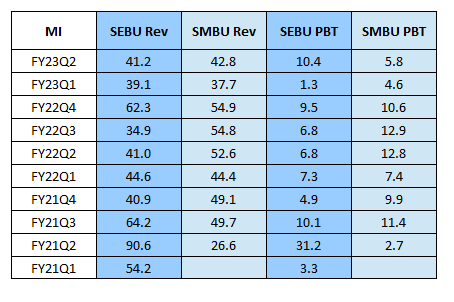

MI is not much better than Gtronic.

Its FY23Q2 looks impressive on surface but it's mainly contributed by the RM15mil forex gain in the quarter alone.

However, total revenue does pick up a bit from preceding quarter from RM76.8mil to RM84.1mil, while the PATAMI soared to RM22.7mil (EPS 2.54sen) from 6.4mil because of the massive forex gain.

Anyway, another 2sen of dividend is declared as the first dividend of FY23. It paid total 4sen for previous FY22.

Rhonema's FY23Q2 result was not good as well.

Both revenue (RM45.2mil) and PATAMI (RM2.57mil, EPS 1.16sen) dropped QoQ.

There are not much explanation given in the report and I guess things will continue to be hard for it in the rest of 2023.

LEESK's FY23Q2 revenue and net profit of RM31.1mil & RM2.64mil (EPS 1.64sen) were a bit disappointing.

Revenue picked up by 4.7% but net profit dropped by 23% compared QoQ.

Domestic sales increased by 6.5% compared YoY and the same old story of poor export sales continue.

The management seems to bet on the collaboration with Cuckoo but there are always some impairment of receivables coming from it.

This time there was an RM0.33mil impairment which was quite significant in view of its low profit.

Nevertheless, management did guide earlier that export sales have improved in the second half of FY2023 with some orders from new customers.

Thus, shareholders should remain hopeful for a better second half.

The 6-state election has just been concluded on 12th Aug 2023. Each coalition won 3 states each as expected.

In summary, current "unity government" is still rather unstable and this is no good news to the stock market at all.

No comments:

Post a Comment